Following the introduction of the personal savings allowance (PSA) in 2016, many savers have been able to save tax-efficiently without an ISA due to low interest rates.

It’s important to review your savings plans to make sure you’re making the most of your tax-free allowances and saving tax-efficiently.

Below we’ll explain how the PSA works, what an ISA is, and why there are a number of reasons to consider them as part of your tax-efficient savings options.

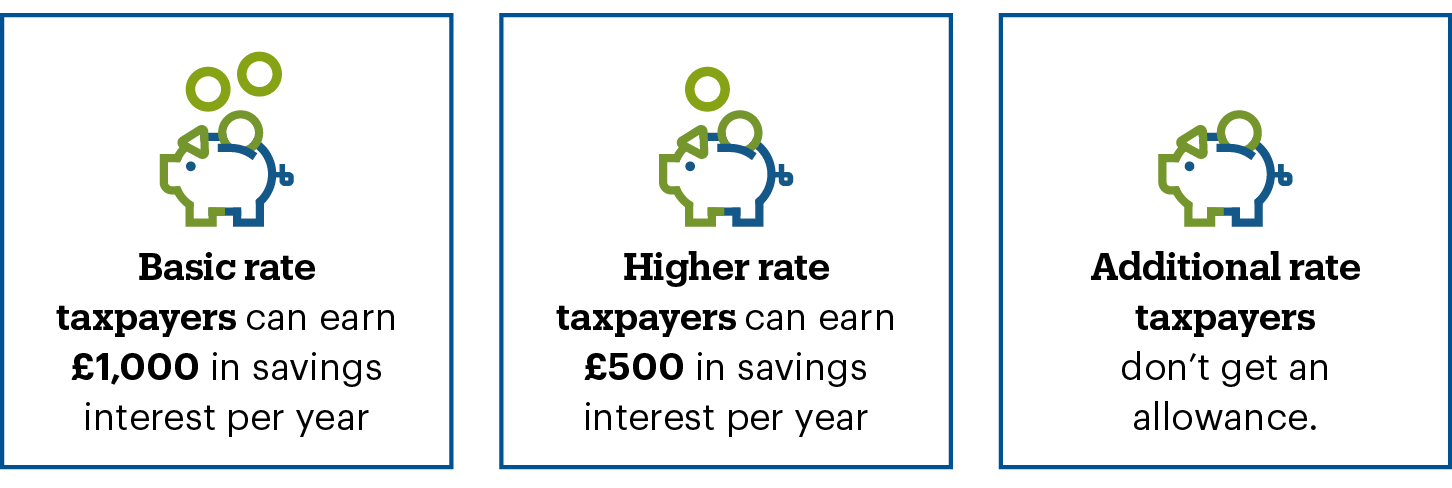

What is the Personal Savings Allowance (PSA)?

The PSA is a tax-free allowance which lets you earn interest on your savings each year, up to a threshold, without paying tax on the interest earned, depending on the rate of income tax you pay.

If you earn less than £17,570 per tax year, you may be able to earn more savings interest without paying tax. Please see to the Gov.uk website for more information.

HM REVENUE AND CUSTOMS PRACTICE AND THE LAW RELATING TO TAXATION ARE COMPLEX AND SUBJECT TO INDIVIDUAL CIRCUMSTANCES AND CHANGES WHICH CANNOT BE FORESEEN.

What is an ISA?

ISA stands for Individual Savings Account and is a tax-free way of saving. Currently you can deposit up to £20,000 into ISAs each tax year, which runs from 6th April to 5th April each year, and you’ll pay no tax on the interest you earn.

If you’re interested in opening an ISA, you can view our existing range here.

Can I use the Personal Savings Allowance and my ISA allowance?

Yes, you can make use of both allowances and this guide can help you make the most of each.

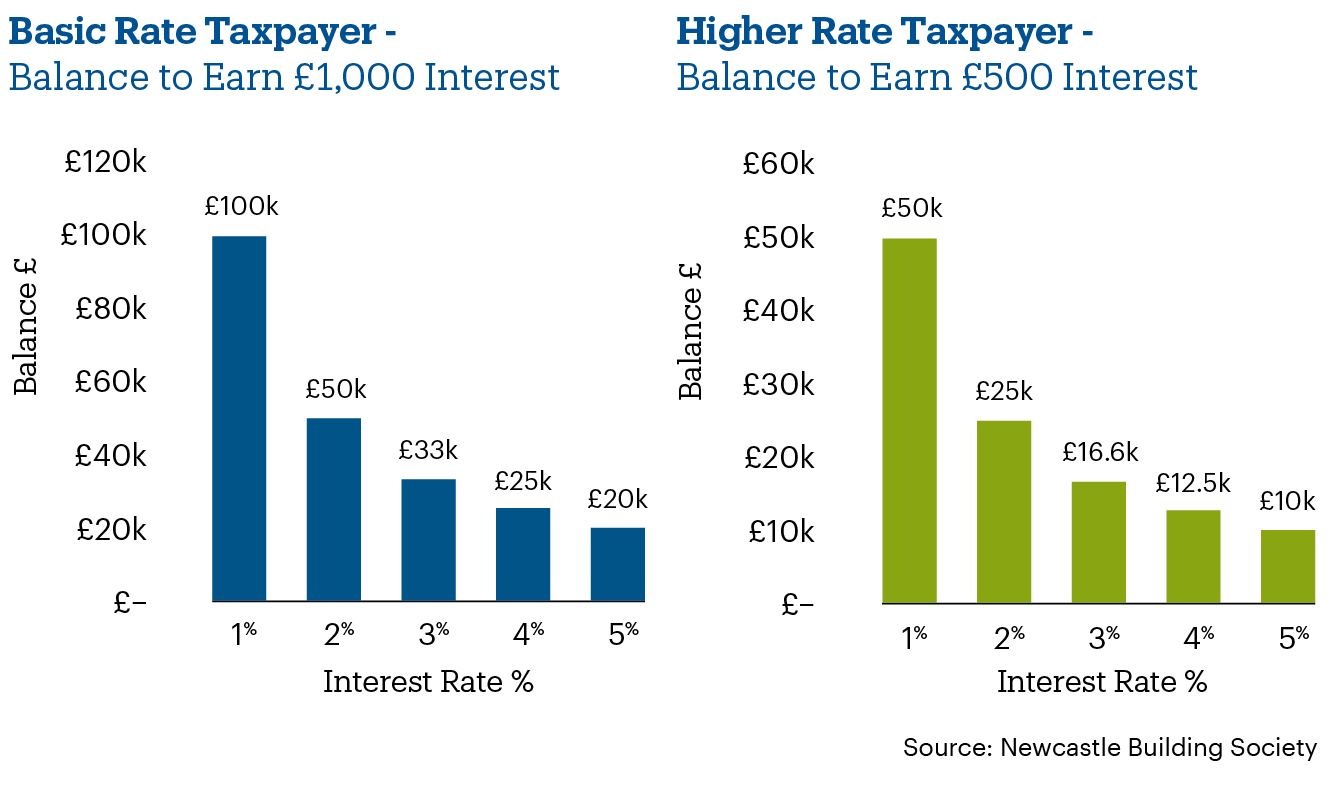

How much do I need to save before I reach my PSA limit?

The charts below show how much you would need to save at interest rates between 1% and 5% to reach your PSA limit.

Please note if you invest in a non-ISA fixed term savings account with a term longer than 1 year, any interest that is paid into the account will count towards your PSA in the tax year when the funds become accessible, i.e. upon maturity.

What are the benefits of ISAs compared to the PSA?

- Money in an ISA will always be protected from tax, year after year, for as long as the money stays in an ISA.

- Your ISA allowance renews each new tax year – so you can build up a bigger tax-free pot over time.

- You will always be able to access your ISA funds, however, some ISAs may carry a penalty for this.

- The value of your ISAs can be transferred to your spouse or civil partner if you pass away, protecting your tax-free savings.